Ukrainian Reconstruction

Who Rebuilds — and Who Profits?

On March 25, 2026, a joint U.S.-Ukrainian board of directors approved an equity investment in a small Lviv-based startup called Sine Engineering. The company makes GPS-independent navigation software for drones, technology used by over 150 Ukrainian drone manufacturers on the front lines. It beat out more than 200 applicants. The investment came from the U.S.-Ukraine Reconstruction Investment Fund, or URIF, the financial vehicle created by last year’s minerals deal between Washington and Kyiv.

That deal, signed on April 30, 2025, after the United States froze military aid and cut off intelligence sharing to pressure Ukraine into terms, was called “neocolonialism” and “pure extortion” by many observers. One year later, its first tangible product is an investment in Ukrainian-made technology that is saving Ukrainian lives. That contradiction is at the center of a $588 billion question: Who is actually going to rebuild Ukraine, under what terms, and who walks away with the profit?

Arrangements for the Deal

Start with the structure. The minerals agreement establishes a joint investment fund (URIF) seeded with $150 million, split equally between the U.S. (through the Development Finance Corporation, or DFC, the government’s development bank for private-sector investment in developing countries) and Ukraine. The fund is governed by a six-member board, three American, three Ukrainian. It targets investments in critical minerals, energy, transport and logistics, information technology, and emerging technology.

Ukraine contributes 50 percent of all revenues from newly issued licenses for critical minerals, oil, and gas exploration. Existing revenue streams: Naftogaz (Ukraine’s state oil and gas company) and Ukrnafta (its largest publicly traded oil producer), are excluded. The deal covers 55 named minerals plus oil and natural gas, with provisions to add more by mutual agreement. For the first ten years, all profits stay in Ukraine. After that, profits may be distributed between the partners. Ukraine retains full ownership of its resources and determines what gets extracted and where. On paper, the structure looks reasonable. A 50/50 split and a decade of reinvestment all honor Ukrainian sovereignty over extraction decisions. But that’s not the full story.

The terms arrived through coercion. In February 2025, newly confirmed Treasury Secretary Scott Bessent presented President Zelenskyy with a demand: 50 percent ownership of Ukraine’s rare earth minerals, framed as repayment for previously provided military assistance. When Zelenskyy balked, the United States halted military aid and stopped sharing intelligence, in the middle of an active war.

U.S. Special Envoy Keith Kellogg later suggested these measures were intended to bring Ukraine to the table. The diplomatic term for this is “leverage.” A less diplomatic term exists. Ukraine’s parliament ratified the agreement unanimously on May 8, 2025. Unanimity in a wartime parliament facing an aid cutoff is not enthusiasm.

The Just Security legal analysis posed a direct question: “Is the U.S. procuring a minerals treaty with Ukraine by use of force?” Whether the answer is technically yes or technically no, the optics are not ambiguous. The country providing weapons to keep another country alive used those weapons as bargaining chips to secure long-term access to that country’s natural resources.

What Does $588 Billion Buy

The World Bank’s most recent assessment, released February 23, 2026, puts Ukraine’s total reconstruction and recovery cost at $588 billion over the next decade, nearly three times Ukraine’s estimated 2025 GDP. Direct damage has reached $195 billion. Fourteen percent of all housing has been damaged or destroyed, affecting more than three million households. The 2026 reconstruction priority list totals more than $15 billion, covering destroyed housing, demining, and economic support programs.

Against that $588 billion need, the URIF’s $150 million seed capital is a rounding error, 0.025 percent of the total. The fund plans three investments in 2026. It first went to a company that makes drone navigation software. The scale mismatch is enormous. So where does the real money come from?

Corporate Contract Lineup

The answer is American financial and industrial capital, positioned at every level of the reconstruction apparatus.

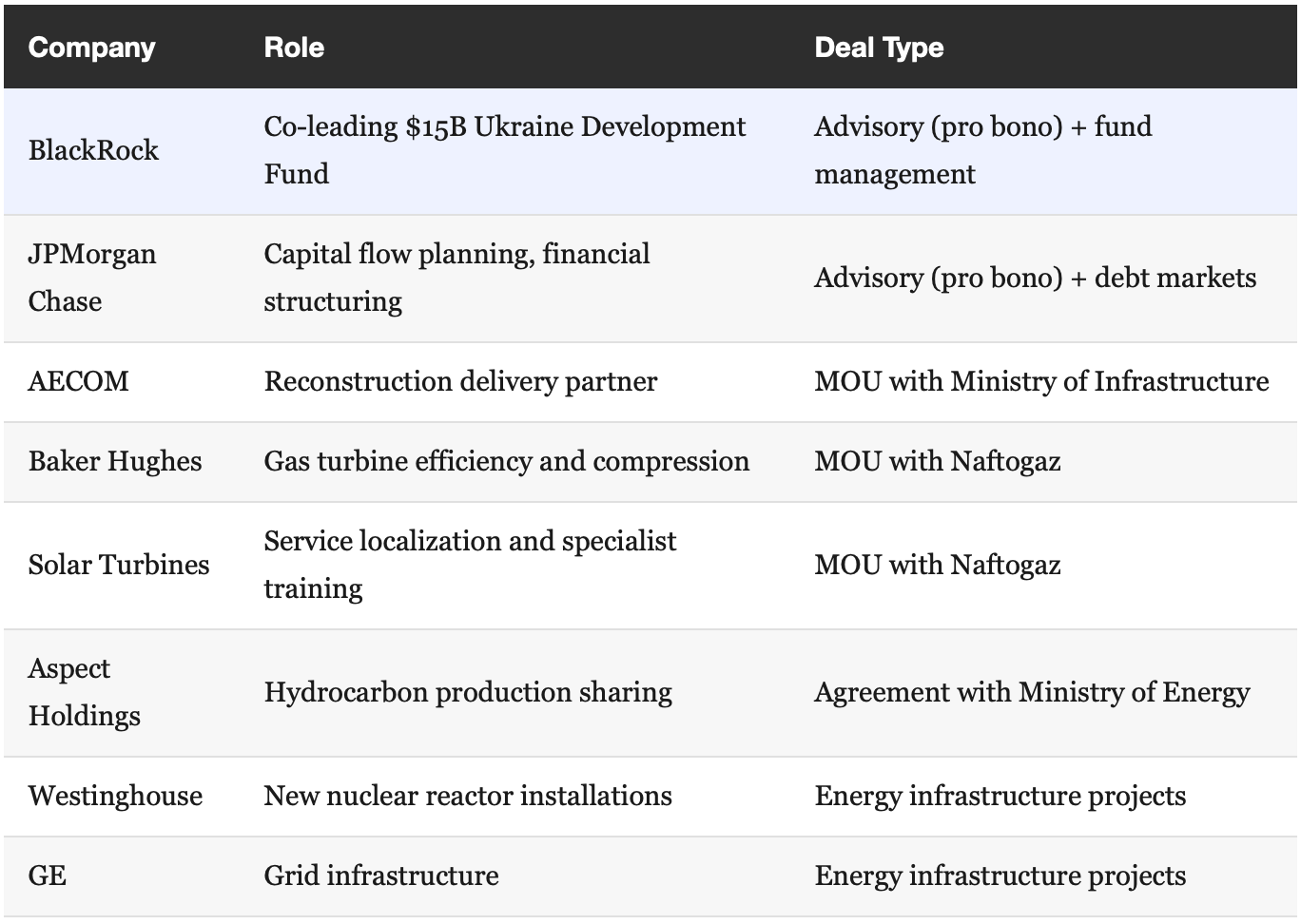

BlackRock was hired by Ukraine in November 2022 to attract reconstruction capital. JPMorgan joined in February 2023 for its debt markets expertise. Both are working pro bono; for now. Their Ukraine Development Fund has gathered $500 million in committed capital and targets $15 billion total. In March 2026, Ukraine’s Energy Minister signed new agreements with Baker Hughes, Solar Turbines, and Aspect Holdings in Washington, with the DFC exploring $1.4 billion in credit support for energy equipment. These companies bring real capabilities Ukraine needs, not simply predatory goals. But the pattern is familiar: American capital arrives first, secures the contracts, and sets the terms while the client country has limited bargaining power.

Iraqi Analogy

Americans have seen this pattern before. After the 2003 invasion of Iraq, Halliburton’s subsidiary Kellogg, Brown & Root received $11.4 billion in contracts to rebuild Iraq’s oil infrastructure, through a $7 billion no-bid contract. Bechtel received $2.9 billion for utilities, roads, and schools. More than 70 American companies won up to $8 billion in postwar contracts over two years. The contracts operated on a cost-plus basis, the more a company spent, the more it earned. Military auditors caught Halliburton overcharging the Pentagon for fuel deliveries.

The Ukraine arrangement is different. The funding comes from private capital and resource revenues, not taxpayer appropriation. The contracts are investment partnerships, not cost-plus billing. The oversight includes equal Ukrainian board representation. But the underlying dynamic resonates. There is a country in crisis. American firms are well-positioned. Then terms are negotiated when one side has far more power than the other. While the details differ, the inexorable pull is the same.

Marshall Plan?

Comparison to the Marshall Plan comes up in nearly every discussion of Ukraine reconstruction. The comparison flatters the current effort more than it should. The Marshall Plan was 90 percent grants, frontloaded at roughly 2 percent of U.S. GDP in its first year. It was funded by American taxpayers, implemented after the fighting stopped, and designed to build self-sufficient economies.

The Ukraine model is the inverse. Investment-based, not grant-based, returns flow to investors. It operates during an active war. It is funded by private capital seeking profit. And Ukraine’s own resource revenues flow into a joint fund where the United States holds equal governance authority for at least a decade. The Peterson Institute noted that “any future Marshall Plan for Ukraine will probably be European.” The current U.S. approach is a business arrangement. Calling it a Marshall Plan obscures the truth of the matter.

It Could Have Been Green

Here is where the deal’s long-term implications get uncomfortable, and where observers in the sustainability space will recognize the dynamics. Global Witness estimated that the U.S. could capture up to $353 billion in Ukrainian oil and gas revenues under the deal’s terms. The hydrocarbon production-sharing agreements signed in March 2026 reinforce the fossil fuel pathway. Ukraine is being rebuilt around oil, gas, and mineral extraction.

An excellent alternative exists. Renewables could power almost 80 percent of Ukraine’s economy by 2050. Wind potential: 180 gigawatts onshore, 251 gigawatts offshore. Solar: 39 gigawatts. Another study calculated that 1 percent of Ukraine’s land area, used for solar and wind, could meet 91 percent of its energy needs. And on the money side prioritizing decarbonization in reconstruction would require only 5 percent more capital investment than the fossil fuel pathway.

Five percent is the cost difference between extraction dependence and a modern energy system. And the returns tell the same story. 2024 data showed that 91 percent of new renewable projects commissioned that year were cheaper than any new fossil fuel alternative. Solar was 41 percent cheaper than the lowest-cost fossil option; onshore wind was 53 percent cheaper. Globally, renewables avoided $467 billion in fossil fuel costs in 2024 alone. Thorough analysis of publicly traded energy companies found that renewable power portfolios generated higher total returns than fossil fuel portfolios across both developed and developing economies. The financial case for green reconstruction is settled, not aspirational any more.

The minerals deal pushes toward extraction anyway, not because it is economically optimal, but because the companies positioned to profit are extraction companies. The supreme irony is that the critical minerals in this deal, lithium, titanium, graphite, rare earths, are the building blocks of renewable energy technology. The deal extracts them to sell to others that are retooling their energy systems, not to benefit Ukraine’s (or the US’s) long term energy needs. In some senses, this is the imperial model retooled for modern times, with a dash of obtuse lack of imagination.

The Sine Engineering Complication

And yet, the first investment did go to Sine Engineering. Sine Engineering is the Lviv-based startup founded in 2022. It develops and produces satellite-independent navigation software that allows drones to fly without GPS, a critical capability given Russia’s electronic warfare battlefield counter measures. Its components are used by over 150 Ukrainian drone manufacturers. Sine is a Ukrainian company, founded during the war, building defense technology, selected competitively from 200+ applicants, funded by a joint board with equal Ukrainian representation. It’s not Halliburton.

An April 2026 assessment acknowledged that while academic opinion remains skeptical of the deal’s origins and structure, “its structure and goals are seeds of the same strategic logic, one that serves the interests of both the United States and Ukraine.” The fund got off to what might best be termed as “an energetic start.”

Does one good investment redeem a deal born from coercion? No. But it complicates the narrative that the entire arrangement is extractive. The question is whether Sine Engineering represents the rule or the exception; whether the fund will continue investing in Ukrainian innovation or will shift toward the extraction projects that generate revenue for the 50/50 split. Two more investments are planned for 2026. What they fund will tell us more than any policy paper.

What the Evidence Says

This deal was made badly and may yet work usefully. The United States froze military aid to a country fighting for survival and extracted resource concessions as the price of turning it back on. The structure channels half of new mineral and energy revenues into a fund where Washington holds equal governance power. The corporate lineup, BlackRock, JPMorgan, AECOM, Baker Hughes, is American. The energy agreements signed in March 2026 favor fossil fuels despite renewables being cheaper by 40 to 50 percent. A $150 million seed fund is a rounding error against $588 billion in reconstruction needs, but it establishes the governance template for everything that follows. The origins of this arrangement are coercive, and the structure favors American capital.

And within that structure, the first investment went to Sine Engineering, a Ukrainian company, founded during the war, making technology that saves Ukrainian lives, selected competitively from 200 applicants by a board with equal Ukrainian representation. Ukraine retains ownership of its resources. The ten-year reinvestment lock prevents early profit-taking. The deal excludes existing revenue streams. The alternative to this imperfect arrangement was not a better deal, it was no American investment at all, leaving Ukraine more dependent on European institutions and a shattered domestic economy.

This is not a novel approach. Beijing has spent a decade running a version of it through the Belt and Road Initiative, lending billions to developing nations for ports, railways, and power plants, then securing long-term access to critical minerals as repayment. China now controls the majority of global refining and processing capacity for rare earths, lithium, cobalt, and graphite. An economic review of over 1,000 Chinese loans found the “debt trap” label was overstated; most borrowing nations were not deliberately ensnared. But the structural outcome is consistent: countries that traded resource access for infrastructure investment found themselves locked into commodity-export dependence, vulnerable to price swings, and reliant on Chinese processing capacity they never built domestically. The U.S.-Ukraine minerals deal follows the same pattern. Whether Washington learned anything from watching Beijing run it first, or simply wanted a turn, depends on what the fund does next.

Stoic Moments

“No man is free who is not master of himself.” — Epictetus

Epictetus was born a slave and lived a life under the control of others. He knew something about agreements made under duress. His insight is practical: mastery is about what you do within the constraints you face.

Ukraine signed this deal with limited options. The question now is whether Ukrainian institutions, the board members, the regulators, and the parliament, exercise mastery within the structure they accepted. The fund’s first investment suggests someone is trying. Whether that holds through the next $588 billion is the test. Two more investments are planned for 2026. They will tell us whether this fund builds Ukraine’s economy or strips it. Watch them.

Need to Do Something?

Support organizations tracking reconstruction accountability: the Project on Government Oversight (POGO), which documented Iraq reconstruction fraud; the International Consortium of Investigative Journalists (ICIJ), which covers the money trail in conflict reconstruction; and Global Witness, which tracks natural resources, conflict, and corruption.

And closer to home: strengthen communities through mutual aid. Donate food, volunteer, contribute funds. Clean up the garden, plan for spring, check on neighbors, and care for those close. Those daily acts of civic life remain the foundation of a functioning democracy, especially when the government has other priorities.

Countdown

Countdown to the national mid-term elections, when the public can express its opinions about the performance of Congress: 214 Days

Countdown to the national presidential elections, when the public can express its opinions about the performance of Congress and the President: 949 Days

PBS News. (2025, April 30). What’s in the minerals deal Ukraine signed with the United States? PBS NewsHour.

CSIS. (2025). Breaking Down the U.S.-Ukraine Minerals Deal Center for Strategic and International Studies.

CSIS. (2026, February 9). Six Months Since the U.S.-Ukraine Minerals Deal Was Signed — What Now?Center for Strategic and International Studies.

Ellis, J.C. (2026, April). From Theory to Reality: Evaluating the U.S.-Ukrainian Minerals Deal War on the Rocks.

TIME. (2026). The U.S.-Ukraine Minerals Pact Is Still a Bad Deal TIME.

Global Witness. (2025). Trump’s minerals deal: Bad for Ukraine, bad for climate Global Witness.

Global Witness. (2025). US could seize $353bn of Ukraine oil and gas money in deal Global Witness.

Just Security. (2025). Is U.S. Procuring a Minerals Treaty with Ukraine by Use of Force? Just Security.

World Bank. (2026, February 23). Updated Ukraine Recovery and Reconstruction Needs Assessment Released World Bank Group.

Kyiv Independent. (2026, March 25). Exclusive: Ukrainian defense tech firm lands first US-Ukraine minerals fund deal Kyiv Independent.

Kyiv Post. (2026). Ukraine-US Reconstruction Fund Approves First Investment in Drone-Tech Firm Kyiv Post.

U.S. Department of the Treasury. (2026). URIF Announces First Investment, Strengthening Ukraine’s Security and Unlocking New Emerging Technology for the United States and Allies U.S. Treasury.

DFC. (2026). DFC Announces U.S.-Ukraine Reconstruction Investment Fund Fully Operational U.S. International Development Finance Corporation.

Ukrainska Pravda. (2026, March 25). Ukraine’s energy minister outlines US hydrocarbons and energy equipment agreements Ukrainska Pravda.

BlackRock/JPMorgan. (2024). BlackRock and JPMorgan are backing a $15 billion investor fund to rebuild Ukraine Quartz.

ICIJ. (2003). U.S. contractors reap the windfalls of post-war reconstruction International Consortium of Investigative Journalists.

PIIE. (2023). Lessons from the past for Ukrainian recovery: A Marshall Plan for Ukraine Peterson Institute for International Economics.

UNECE. (2024). Renewables could power almost 80% of Ukraine’s economy by 2050 United Nations Economic Commission for Europe.

ETH Zurich. (2024). How Ukraine can rebuild its energy system ETH Zurich.

IRENA. (2025, July). 91% of New Renewable Projects Now Cheaper Than Fossil Fuels AlternativesInternational Renewable Energy Agency.

Imperial College London. (2024). Clean Energy Investing: Global Comparison of Investment ReturnsImperial Business School.

Chatham House. (2026, March). America needs partners to challenge China’s critical mineral chokeholdChatham House.